New Fire Insurance Resources To Keep Your Clients Informed

by

California Insurance Commissioner Ricardo Lara and United Policyholders, a nonprofit that advocates on behalf of consumers, recently presented an insurance townhall briefing for REALTORS® to learn about California’s property and casualty insurance market and how the new Safer From Wildfires regulations can help homeowners and businesses qualify for insurance discounts.

Watch a replay of the briefing at your convenience (right).

C.A.R. and CCAR will continue to provide new information and resources as they become available. Click on the flyers below to learn more.

NEW RESOURCES

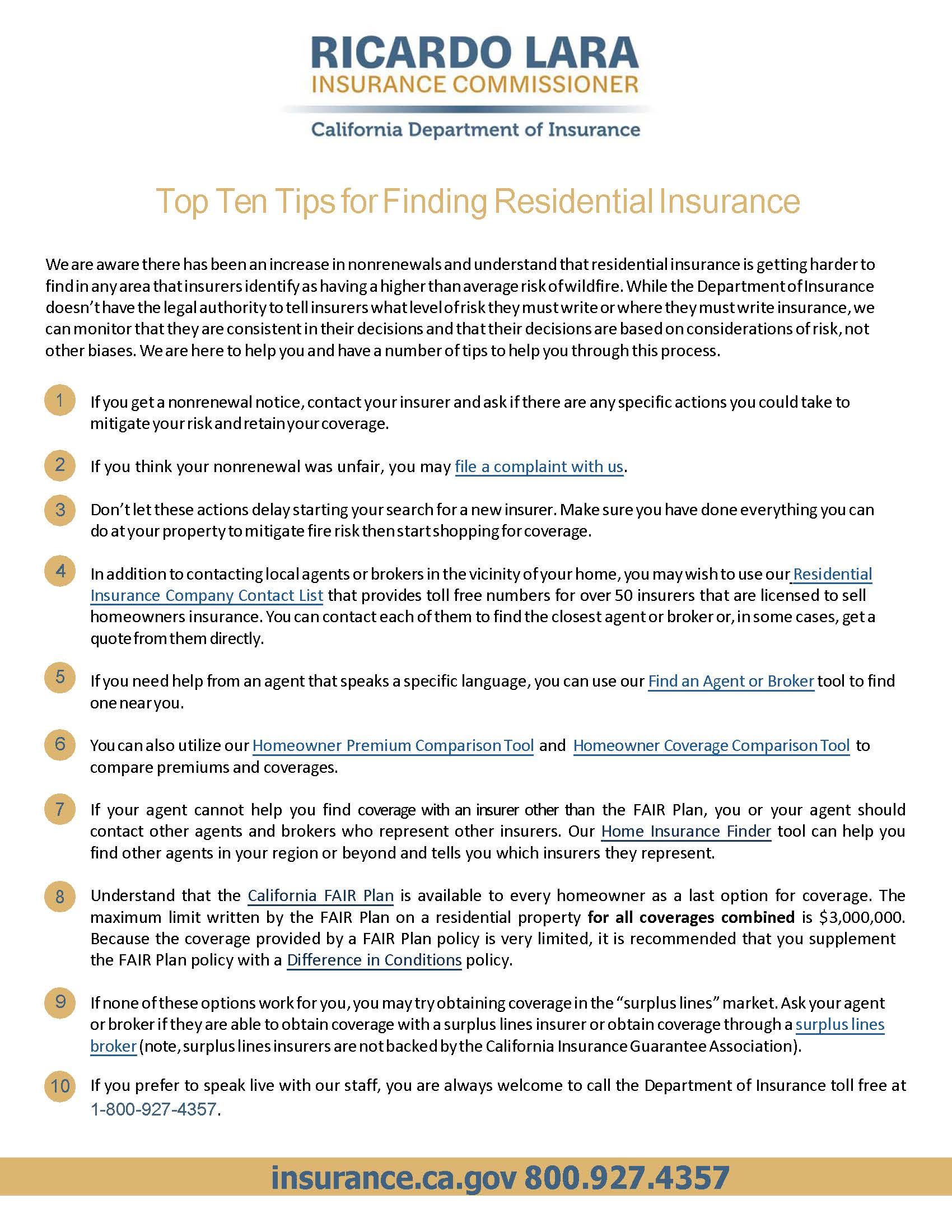

Top 10 Tips For Finding Residential Insurance

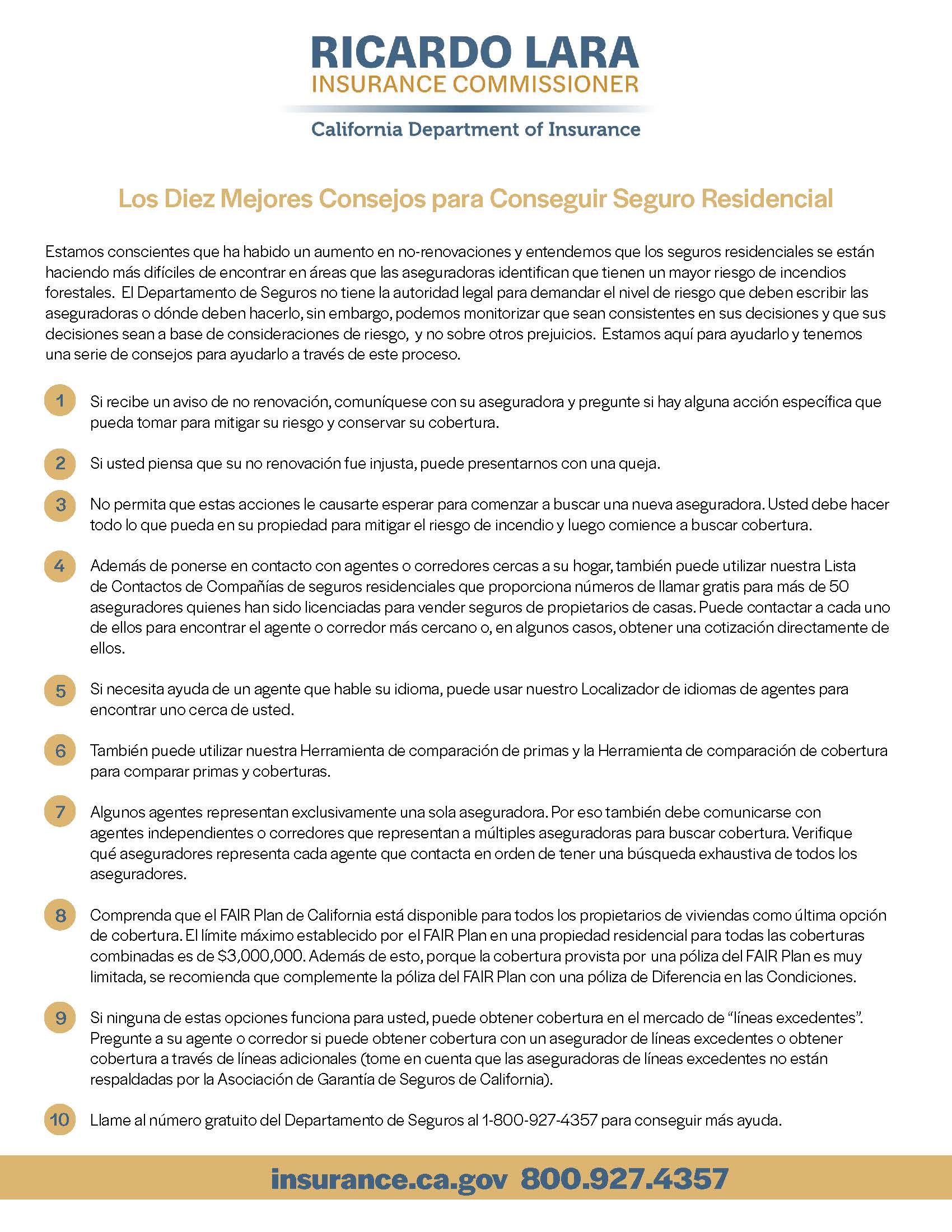

Top 10 Tips For Finding Residential Insurance – Spanish

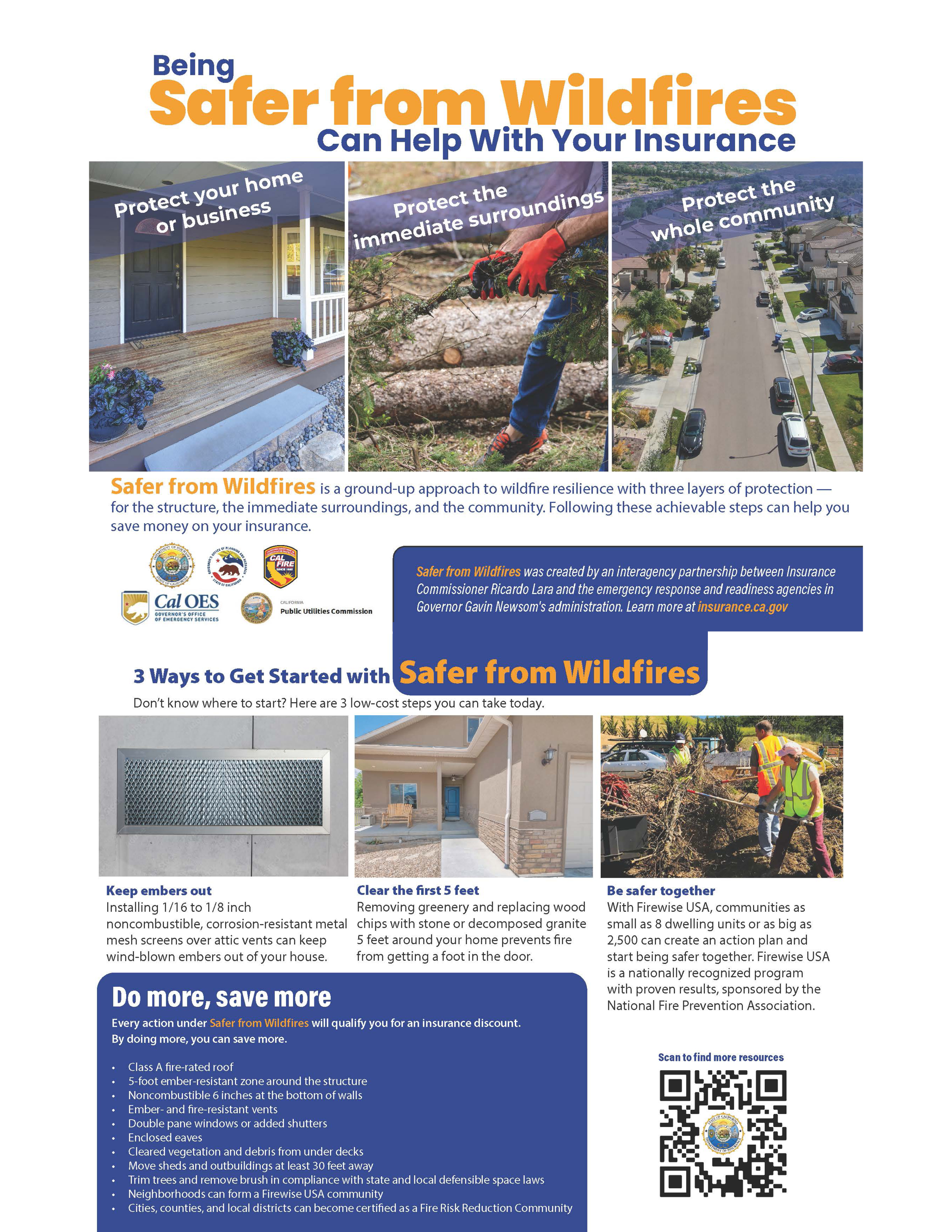

Being Safer From Wildfires Can Help with Insurance

How to Find (or Keep) Fire Insurance

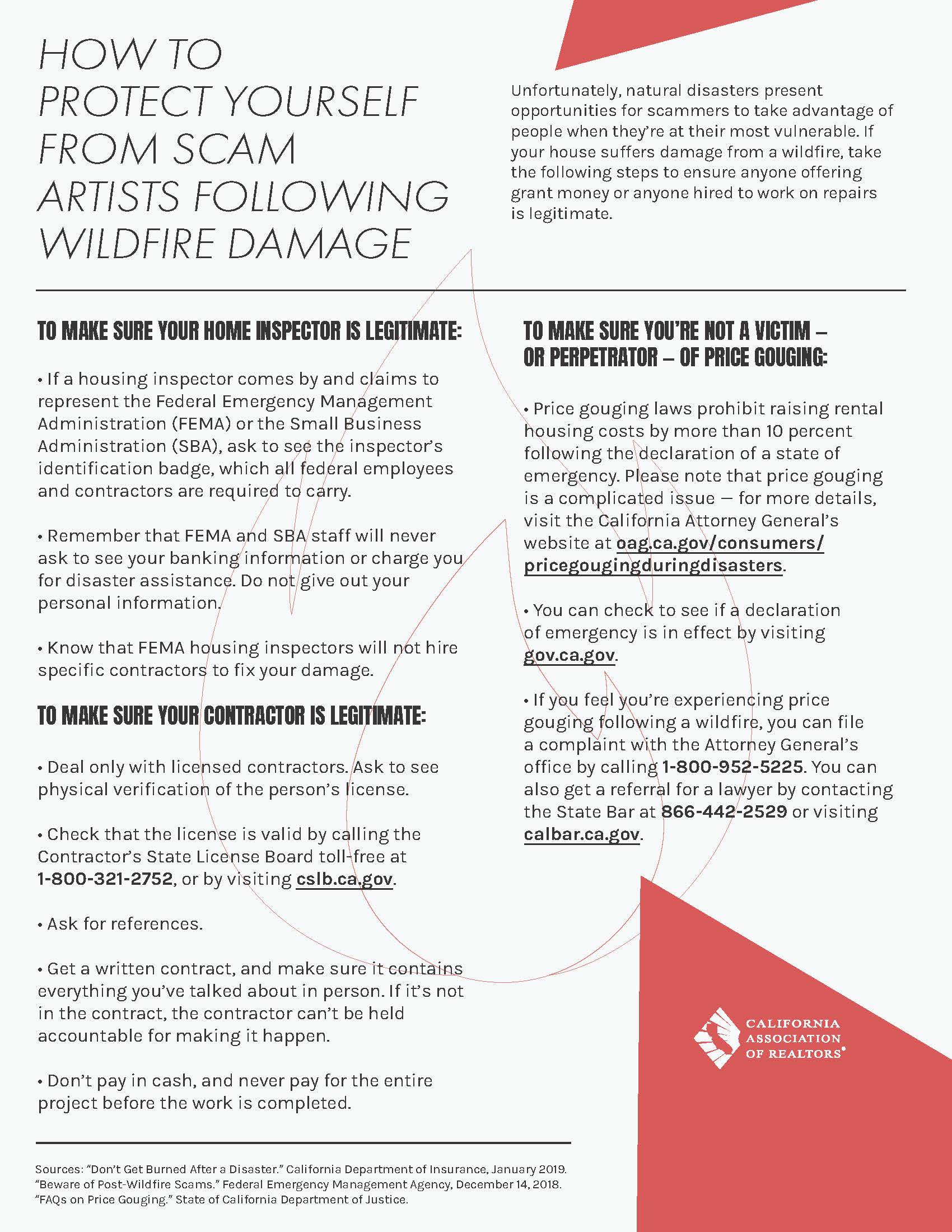

How To Protect Yourself

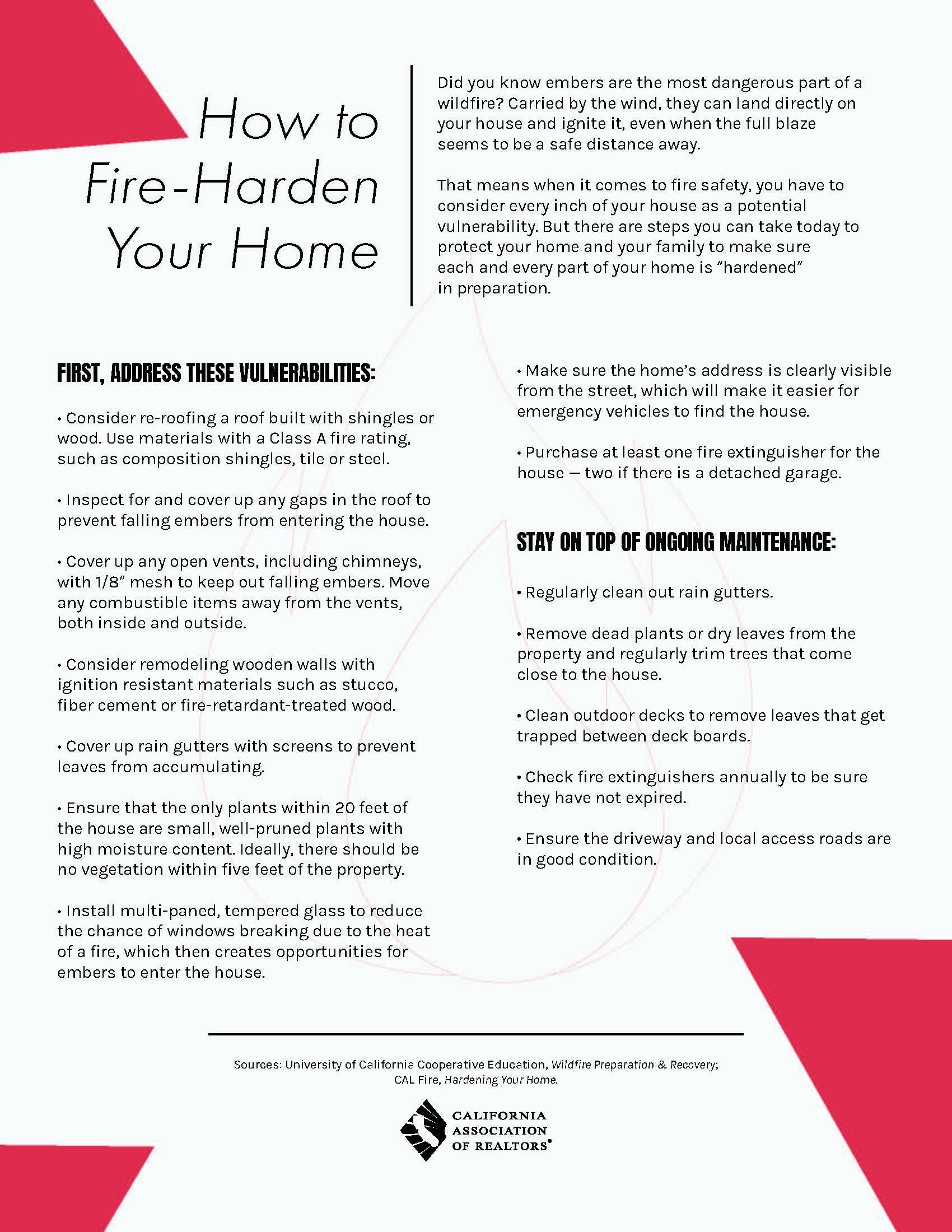

How to Fire Harden-Your Home

There is no fire insurance contingency in the Residential Purchase Agreement Investigating the availability and cost of fire insurance is the responsibility of a buyer. A buyer who is not satisfied with either would ordinarily have the right to cancel a contract but only during the buyer’s investigation contingency. If an offer is made without an investigation contingency, or if that contingency is removed, a buyer who backs out of a contract because of the anticipated cost or availability of fire insurance could be in breach of contract. Even if a loan contingency is still in effect, and the lender refuses to make the loan because the buyer has not acquired a fire insurance policy either because of its costs or coverage, the lender’s failure to loan would be due to the buyer’s affirmative decision and would not justify exercise of the loan contingency.

The impact of California wildfires has impacted the cost and availability of fire insurance. Buyers are advised to investigate the cost and availability of fire insurance before making an offer, just like many buyers investigate loan rates and terms, and obtain a prequalification or preapproval from a lender or loan broker in advance of making an offer. Buyers should discuss fire insurance possibilities with an insurance agent. Factors to consider are the location of property in a state or local fire zone, fire hardening of potential property, proof of compliance with defensible space laws (See Quick Guide and Q&A on Defensible Space Laws), whether an insurer is admitted in California, and the scope of coverage available, including policies from the California Fair Plan.

A buyer who acquires fire insurance to complete a property purchase cannot let that policy lapse without exposing the buyer to financial risk. If the buyer has obtained a loan secured by the property, the lender will typically have a forced-payment clause in the loan documents which allows the lender to acquire fire insurance on the owner’s behalf, at the owner’s expense, if the owner’s fire insurance policy is no longer effective because the owner stops making payments, or the fire insurance company terminates coverage for any other reason. Policies obtained through a forced-payment clause are usually designed to primarily protect the lender’s secured interest, and not the owner’s ability to fully recoup losses in the event of a fire. Such policies can be expensive and have limited coverage. Even if a property is not secured by a loan, the buyer is exposed to all of the losses and costs to rebuild in the event of a fire if there is no fire insurance policy in effect at the time of fire.

There are restrictions on an insurance company’s right to terminate coverage or “non-renew” an existing policy as well minimum rights applicable to temporary relocation and time to rebuild. In an effort to assist homeowners, the California Legislature has enacted laws that require fire insurers (i) to continue and/or renew coverage for at least one year from the date of a declaration of emergency (Insurance Code § 675.1), (ii) to pay for necessary additional living expenses for up to 24 months (Insurance Code § 2060), (iii) to allow owners 36 months to rebuild because of the difficulty in finding coverage and contractors after a widespread wildfire (Insurance Code § 2051.5). If the fire insurance carrier is not admitted in California, these Department requirements may not apply. Fire insurance companies can terminate a policy for non-payment of the premium.

Platinum Partner, NAR Corporate Ally Program

Platinum Partner, NAR Corporate Ally Program CCAR is proud to be a RESO Platinum Certified MLS, the highest level of certification available.

CCAR is proud to be a RESO Platinum Certified MLS, the highest level of certification available.